Flat Fee Lending Business: Startup Financial Model

![flat fee lending business startup financial model 1]()

![flat fee lending business startup financial model 2]()

![flat fee lending business startup financial model 3]()

![flat fee lending business startup financial model 4]()

![flat fee lending business startup financial model 5]()

![flat fee lending business startup financial model 6]()

![flat fee lending business startup financial model 7]()

![flat fee lending business startup financial model 8]()

![flat fee lending business startup financial model 9]()

![flat fee lending business startup financial model 10]()

![flat fee lending business startup financial model 11]()

![flat fee lending business startup financial model 12]()

![flat fee lending business startup financial model 13]()

![flat fee lending business startup financial model 14]()

![flat fee lending business startup financial model 15]()

![flat fee lending business startup financial model 16]()

![flat fee lending business startup financial model 17]()

![flat fee lending business startup financial model 18]()

Recent Upgrades: Added three statement model (IS,BS,CF) and a cap table.

A flat fee lending business means the customer repays a certain defined percentage of the principal borrowed instead of a regular monthly interest rate. No compounding interest happens within this type of financing. There are various ways the flat fee and principal can be paid back and the dynamic nature is captured in the model.

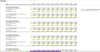

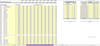

The model can handle two repayment methods (yes/no toggle):

1. The total principal borrowed and fee can be fully repaid at the end of the loan term.

2. The total principal borrowed and fee can be evenly repaid over the course of the loan term.

I have seen both methods uses for actual startups.

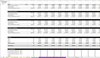

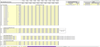

The user can configure up to four different loan term configurations as well as a dynamic start month for each. The following can be adjusted over 10 years:

- Monthly Loan Volume

- Flat Rate Fee

- Average Loan Amount

- Loan Term (months)

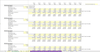

The other unique aspect about this business is that often times a lender of flat fee loans will borrow the cash required to make such loans from a traditional senior debt facility that has an APR and monthly interest repayment. The goal is to make a great margin between the interest paid back for senior debt service and the fees collected from all the loans.

As you can see, this gets complicated fast and a financial model that captures all the nuance can be helpful in setting loan terms, fee rates, and planning out general funding needs as well as expected total returns over time.

Also, the money borrowed can only be borrowed to fund the direct loan activity and not operating expenses. Formulas were used to take any negative cash flow from lending activity and assume it is financed (if the senior debt financing toggle is set to 'yes') An APR can be defined in each month as well.

If you don't want to have a senior debt facility to leverage your loan activity, simply select 'no' on the selector and the cash required will flow down to investor / operators. Upon the exit month, all debt automatically gets repaid and this is offset against all loans receivable (per a multiple less any selling fees) to properly forecast a terminal value. This does not have to be in the model and to leave out terminal value, just enter 'NA' in the exit month and neither aspect will flow to cash flow.

The reason why this is populate is that customers easily understand what fee they will be paying, whereas that can be difficult to see at first with traditional loans and often times a flat fee lending operator can secure much cheaper capital (lower interest rates) than what they are collecting on the flat fee. This results in a high margin business if setup right. You need a model to figure this out.

Note, there are also dynamic fixed cost assumptions as well as scaling of customer service reps / sales reps for larger operations.

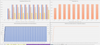

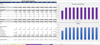

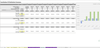

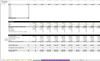

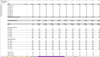

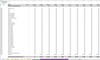

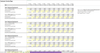

Final outputs include:

- Monthly and Annual Pro Forma and Cash Flow detail

- DCF Analysis (project / investor (if applicable) / operator

- Executive Summary (high level financial line item summary)

- Visualizations of each loan type

Flat Fee Lending Business: Startup Financial Model

Available:

In Stock

$75.00

Recent Upgrades: Added three statement model (IS,BS,CF) and a cap table.

A flat fee lending business means the customer repays a certain defined percentage of the principal borrowed instead of a regular monthly interest rate. No compounding interest happens within this type of financing. There are various ways the flat fee and principal can be paid back and the dynamic nature is captured in the model.

The model can handle two repayment methods (yes/no toggle):

1. The total principal borrowed and fee can be fully repaid at the end of the loan term.

2. The total principal borrowed and fee can be evenly repaid over the course of the loan term.

I have seen both methods uses for actual startups.

The user can configure up to four different loan term configurations as well as a dynamic start month for each. The following can be adjusted over 10 years:

- Monthly Loan Volume

- Flat Rate Fee

- Average Loan Amount

- Loan Term (months)

The other unique aspect about this business is that often times a lender of flat fee loans will borrow the cash required to make such loans from a traditional senior debt facility that has an APR and monthly interest repayment. The goal is to make a great margin between the interest paid back for senior debt service and the fees collected from all the loans.

As you can see, this gets complicated fast and a financial model that captures all the nuance can be helpful in setting loan terms, fee rates, and planning out general funding needs as well as expected total returns over time.

Also, the money borrowed can only be borrowed to fund the direct loan activity and not operating expenses. Formulas were used to take any negative cash flow from lending activity and assume it is financed (if the senior debt financing toggle is set to 'yes') An APR can be defined in each month as well.

If you don't want to have a senior debt facility to leverage your loan activity, simply select 'no' on the selector and the cash required will flow down to investor / operators. Upon the exit month, all debt automatically gets repaid and this is offset against all loans receivable (per a multiple less any selling fees) to properly forecast a terminal value. This does not have to be in the model and to leave out terminal value, just enter 'NA' in the exit month and neither aspect will flow to cash flow.

The reason why this is populate is that customers easily understand what fee they will be paying, whereas that can be difficult to see at first with traditional loans and often times a flat fee lending operator can secure much cheaper capital (lower interest rates) than what they are collecting on the flat fee. This results in a high margin business if setup right. You need a model to figure this out.

Note, there are also dynamic fixed cost assumptions as well as scaling of customer service reps / sales reps for larger operations.

Final outputs include:

- Monthly and Annual Pro Forma and Cash Flow detail

- DCF Analysis (project / investor (if applicable) / operator

- Executive Summary (high level financial line item summary)

- Visualizations of each loan type

Related items

$75.00

$75.00